B2B ecommerce marketplaces are attracting large investments from venture investors excited by the opportunity for high frequency, high value orders in a market that dwarfs B2C ecommerce. While capital is flowing into developed markets, the opportunity in frontier markets can be even larger with limited historical digitalisation of small retailers allowing B2B marketplaces to capture the entire transaction value flow. Having completed our investment in Smart Satu, a B2B marketplace operating in Kazakhstan, Russia and Ukraine, this Sturgeon Insights piece delves into the B2B model and the investment opportunity in frontier markets.

B2B Marketplaces – The Holy Grail of Ecommerce?

Feb 15, 2021

Over the past decade, we as consumers have become so used to ecommerce that it can be difficult to imagine a time without it. The Covid-19 pandemic has only accelerated this trend across both developed and emerging markets: Amazon, AliExpress, Flipkart, Jumia, Mercado Libre, Lazada, Ozon, Souq… the list goes on. These were well known names to consumers and investors before the pandemic and are even more so now. There is, however, an opportunity which is larger and could turn out to be even more lucrative – B2B ecommerce.

The B2B ecommerce opportunity is vast – annual global B2B spending is more than $100 trillion, somewhere in the region of 2-3x the current B2C market. In developed markets, at least 50% of B2B transactions still take place manually via phone, fax, or in-person. In frontier and emerging markets this number is even higher, often more than 90%. The potential for rapid growth from a low base is huge; research by iBe TSD estimates that B2B marketplaces are expected to generate $3.6 trillion in sales by 2024, up from $680 billion in 2018.

There are, however, two fundamental problems that B2B marketplaces need to overcome in order to succeed. Firstly, B2B transactions tend to involve higher average order values (AOVs) than B2C. As a result, the stakes are much higher and one bad transaction can have significant consequences for a business. Quality and trust are therefore crucial, and businesses tend to stick with suppliers and products that they know and understand rather than risking new routes.

Secondly, B2B transactions generally have much more complex workflows: negotiation-based pricing, complicated payment terms, customised orders, and multi-party relationships, amongst other things. These requirements also differ from vertical-to-vertical and country-to-country, meaning it is difficult to copy and paste a solution. This makes it much harder for B2B marketplaces to capture transactions online when compared to their B2C counterparts.

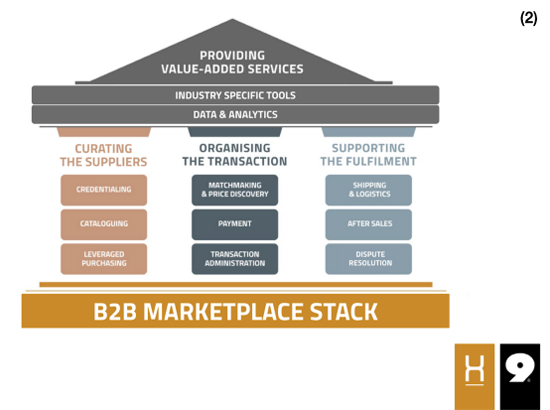

Due to the complexity of the transactions involved, B2B marketplaces must provide a complete solution to streamline and automate the process. Julia Morrongiello from Point9, a VC focused on B2B SaaS and B2B marketplaces, expects that “because of this dynamic, …most B2B marketplaces (particularly those with high AOVs) will be SaaS-enabled by default” (1).From curating the suppliers and organising the transaction through to supporting the fulfilment and providing other ancillary services, there are multiple opportunities for these marketplaces to integrate fully into the transaction flows. In frontier markets where the penetration of business technology is lower, there is an even greater opportunity for B2B marketplaces to capture the value of their clients’ transactions.

Due to the complexity of the transactions involved, B2B marketplaces must provide a complete solution to streamline and automate the process. Julia Morrongiello from Point9, a VC focused on B2B SaaS and B2B marketplaces, expects that “because of this dynamic, …most B2B marketplaces (particularly those with high AOVs) will be SaaS-enabled by default” (1).From curating the suppliers and organising the transaction through to supporting the fulfilment and providing other ancillary services, there are multiple opportunities for these marketplaces to integrate fully into the transaction flows. In frontier markets where the penetration of business technology is lower, there is an even greater opportunity for B2B marketplaces to capture the value of their clients’ transactions.

By solving these two problems, B2B marketplaces can bring significant value for their users: transacting on a digital platform can reduce the time, effort, and cost spent on sourcing and acquiring inventory for retailers, allowing management to focus on growing the business instead. For distributors and suppliers, it can increase turnover with existing clients, open up access to new markets, and reduce costs. These efficiency gains are magnified by the size and frequency of business transactions, and whereas in the past business owners have been slow to adopt technology, the pandemic-enforced lockdown has brought the importance of digitalisation and efficiency more sharply into focus.

As it must develop a platform that can handle the end-to-end transaction process for its users in a simple and efficient manner, B2B marketplaces’ users should be incredibly sticky. That is, once they are comfortable with the platform and trust that it can fulfil their orders correctly and on time, they are unlikely to churn to another solution. While it may have historically delayed the adoption of B2B marketplaces, the hesitancy of retailers to trust new solutions may turn out to be one of their key defensive moats in the future.

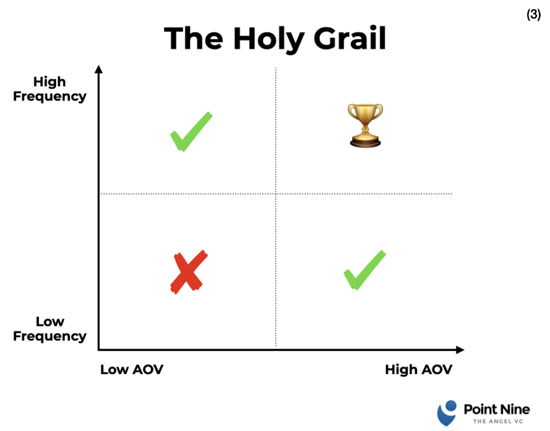

Having built a captive customer base, B2B marketplaces should in theory be able to achieve the “holy grail” of high AOV and high frequency, therefore generating significant GMV through their platform. B2C marketplaces typically occupy the top left or bottom right quadrant of the diagram below. Amazon, for example, has high frequency but low AOV, whereas a property marketplace has high AOV but low frequency.

Having built a captive customer base, B2B marketplaces should in theory be able to achieve the “holy grail” of high AOV and high frequency, therefore generating significant GMV through their platform. B2C marketplaces typically occupy the top left or bottom right quadrant of the diagram below. Amazon, for example, has high frequency but low AOV, whereas a property marketplace has high AOV but low frequency.

However, the revenue model of B2C marketplaces, the GMV “take rate” or percentage of each transaction, does not necessarily translate to the B2B world. Charging a take rate can act as a disincentive for users to transact on the platform, particularly with high AOV. This can be exacerbated by the greater concentration of suppliers and/or demand base on the platform, something that B2C marketplaces don’t face.

Nonetheless, a low take rate can be more than compensated for by the larger size and frequency of transactions. In addition, the B2B marketplace stack as a fully integrated end-to-end solution for its users can diversify revenues with SaaS products. Together with the take rate, this can allow B2B platforms to generate a more diversified and consistent revenue stream than their B2C counterparts.

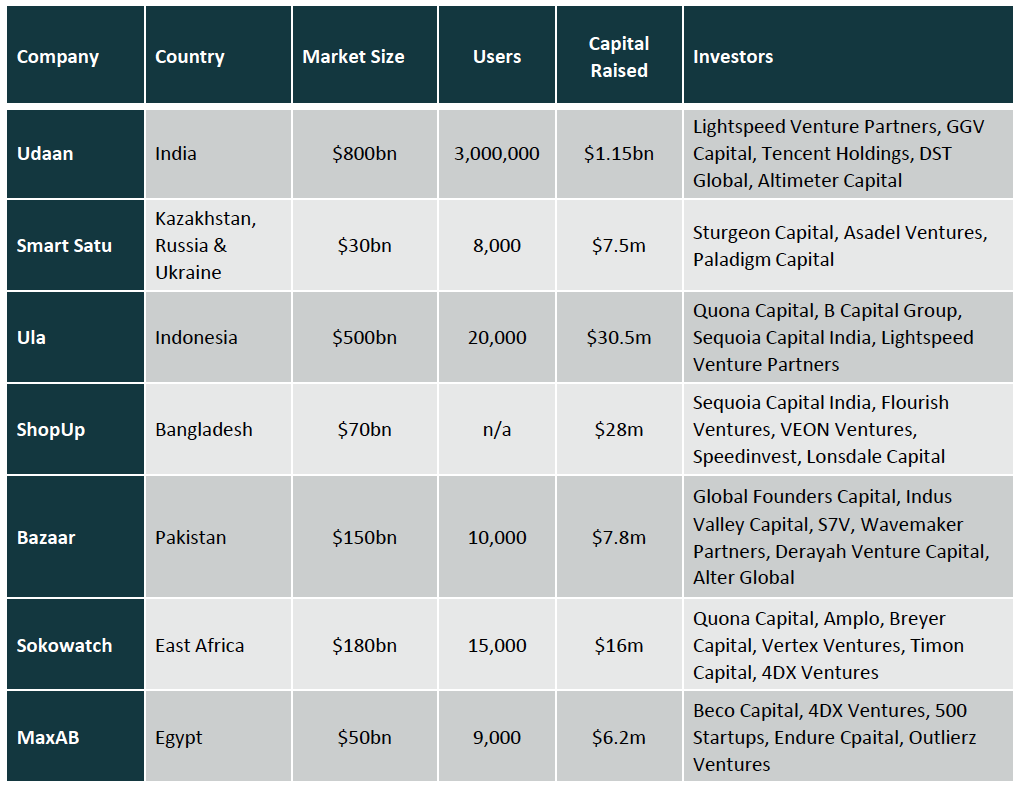

Today there are perhaps two B2B marketplaces which can be considered global: Alibaba and Amazon Business. However, neither of these businesses offers the sort of sophisticated, end-to-end solution outlined above. Nor are they present in the majority of frontier markets. Instead, there are a large number of smaller players operating on a national level looking to capture their domestic market. Several of these have raised significant funding, such as Udaan in India, while others are at an earlier stage of development (See Appendix 1 for details on some of these frontier market players).

There are certain themes common to frontier B2B marketplaces, whether in India, Egypt, Indonesia, or Kazakhstan. Firstly, more than 80% of all retail transactions go through small family-owned shops – in Bangladesh it is as high as 98%! Modern mass retail used in the West has yet to materially penetrate these markets, so there is an even greater capacity for B2B marketplaces to solve the inventory issues that small retailers face. Inventory management can be particularly challenging for these stores who have to order a large number of SKUs from a range of different suppliers and distributors, often with minimum order value requirements. By digitising this process, companies such as MaxAB in Egypt or Bazaar in Pakistan are bringing much greater efficiency to small stores and allowing them to focus on running and growing their business.

The second common theme is that these small merchants have little or no access to credit. When the business is the source of family income, this places a lot of pressure on their working capital cycle. Also, it is very common in these markets for goods to be sold to the end consumer on credit, putting further pressure on the retailer’s cash balance. Rather than ordering more stock when they run out, they often have to wait until they have enough cash from other sales before placing a new order. This limits not just their turnover but also the turnover of the distributors and suppliers.

Marketplaces such as Smart Satu, a Sturgeon portfolio company that operates in Kazakhstan, Russia, and Ukraine, are using the data they have on their clients to offer them working capital finance in partnership with local financial institutions. Access to even a small overdraft facility can allow retailers to dramatically increase their turnover and reduce working capital concerns. Distributors and suppliers benefit from the higher AOV and order frequency, as well as a more formalised relationship with their clients. For banks it opens up a new distribution channel for loans to small businesses, for which they can effectively manage the risk based on the data that the marketplace has on their clients. In this way each member of the ecosystem benefits, and the marketplace can embed itself as the nerve centre for all transactions.

A third issue that plagues this ecosystem is logistics. Distributors have a huge number of small clients spread out around the cities and rural areas of the country. Retailers are usually ordering from a number of different suppliers with independent logistics solutions. This is where marketplaces such as ShopUp in Bangladesh step in, offering an end-to-end solution including logistics that solves the headaches for distributors and retailers alike. Intertwined with the issues of logistics is the prevalence of cash on delivery (COD) payment for items. This is a cost for both sides in the transaction and creates opportunities for fraud. While some marketplaces are streamlining the COD process, others, such as Smart Satu, are removing it altogether. By enabling their retail clients with a corporate bank account, they can both accept non-cash payment from their customers and pay their suppliers digitally.

Given the prevalence of these challenges and the opportunity for those who can solve them, it is not surprising that there has been a large increase in financing for frontier B2B marketplaces. Udaan leads the way having become the fastest unicorn in India; it has raised $1.15bn to date and is valued at $3.2bn. Notable others include Ula in Indonesia, which has raised $30m since its launch in January 2020, and ShopUp in Bangladesh, which raised a $22.5m round in October 2020, taking its total funding to $28m. As these businesses capture market share and more of the value chain, it is likely that we will see more, plus billion-dollar valuations before too long.

For more details on Sturgeon Capital and our frontier markets fund offerings please get in touch

Button

(1) Julia Morrongiello, Point9 – A Primer on B2B Marketplaces: Challenges and Opportunities

(2) Julia Morrongiello, Point9 – The B2B Marketplace Stack

(3) Julia Morrongiello, Point9 – A Primer on B2B Marketplaces: Challenges and Opportunities

Udaan (India)

India has perhaps the most competitive and well-funded B2B marketplace ecosystem in the world. There are an estimated 15 million small and mid-sized retailers that power close to 85% of the country’s retail sales. The proliferation of smartphones and cheap data has made it possible for technology companies to directly access these clients and cut out the middlemen. However, only 3-4% of FMCG products are sold through organised wholesalers. The size of the Indian wholesale market in food and grocery alone is about $600 billion.

Given the size of the opportunity, it is not surprising that there has been substantial capital allocated to B2B marketplaces. The most high-profile start-up is Udaan, which raised a Series D round in December 2020 at a valuation of $2.7bn. Co-founded by three former Flipkart executives, Udaan connects small retailers with wholesalers and traders. Today it serves more than 3 million retailers and small and medium-sized businesses as well as 25,000 sellers across 900 cities. It has signed up thousands of brands, including Coca-Cola, PepsiCo, Boat Lifestyle, Micromax, HP, LG, ITC, HUL, and P&G. Other than the inventory problem, Udaan also helps merchants secure working capital. Small businesses, especially mom-and-pop shops, rely on the money they secure from selling their existing inventory for buying their next batch. Because Udaan is able to see the engagement of different merchants on the platform, it is able to determine to whom it could safely grant working capital.

It is not alone on the market, however. Having completed its acquisition of Walmart’s Indian operations, Flipkart announced the launch of Flipkart Wholesale, aimed at small retailers. Leveraging the existing infrastructure of Walmart, Flipkart Wholesale is now operational in 23 cities and between September and December 2020 , it saw a 75% month on month increase in the number of customers on its platform. Also competing for the B2B market are Reliance Retail through its Jiomart platform and Amazon’s B2B marketplace Amazon Business, along with other venture capital-backed startups such as Jumbotail, Bijnis, and Ninjacart.

Smart Satu (Kazakhstan, Russian & Ukraine)

Smart Satu is a unique B2B platform that combines various players in the fast-moving consumer goods (FMCG) sector. It does this via an application which connects small retailers with suppliers, distributors, and producers and allows retailers to pick the best available price and delivery conditions, thus, improving efficiency and helping business growth. In addition, it partners with banks, where it facilitates the use of cashless payments both on a B2B and C2B basis as well as collecting and analysing the data of its merchant clients. This, in turn, allows the partner banks to offer credit cards with pre-approved working capital loans to merchant clients.

Their ‘win-win’ solution for the ecosystem has allowed the company to partner with thousands of merchants, leading international distributors, international payment systems such as Visa, and leading local banks such as Sberbank. It has already integrated with multinational companies such as Metro and Visa within its current core operational countries (Kazakhstan, Ukraine, and Russia), and plans to expand in the CIS and MENA regions.

Ula (Indonesia)

Founded in January 2020, Ula operates a wholesale e-commerce marketplace to help store owners stock only the inventory they need and grant them with working capital. The company is trying to organize the sourcing and supply chain for small retailers, so there is a one-stop shop for everybody. Despite the pandemic, Ula has made inroads in the Indonesian market last year and today serves more than 20,000 stores. The opportunity in the region is large: retail spending is expected to surpass $0.5 trillion over the next 4 years and traditional in-store retail accounts for nearly 80% of the total retail market. In January 2021, Ula announced its $20m Series A round, which the company will use to develop their technology and expand across the country.

ShopUp (Bangladesh)

ShopUp is targeted at the large network of 4.5 million ‘mom-and-pop shops’, known locally as Mudi Dokaans, in Bangladesh that account for 98% of the country’s retail sector. ShopUp has built what it calls a full-stack business-to-business commerce platform to solve the key problems these small shops face. It provides three core services to neighbourhood stores: a wholesale marketplace to secure inventory, logistics (including last-mile delivery to customers), and working capital.

In October 2020, ShopUp announced that it had raised a new investment round of $22.5 million, co-led by Sequoia Capital India and Flourish Ventures. ShopUp is the first investment by Sequoia Capital India and Flourish Ventures in Bangladesh. This funding will be used to increase the company’s retail reach, deepen partnerships with manufacturers, and focus on building tech-first infrastructure. The company has raised about $28 million to date from investors and merged with Indian ecommerce platform Voonik earlier in the year as it looks to expand its presence outside of Bangladesh.

Bazaar (Pakistan)

Bazaar aims to digitise the $150bn traditional retail market in Pakistan. 95% of the 2 million mom-and-pop grocery stores (called kiryana stores) operate their business offline, yet 80% of kiryana stores have a smartphone. Using the country’s rising mobile adoption, Bazaar is looking to empower the millions of SMEs that dominate the market by providing significant value and convenience through various digital products. Within eight months of launch, Bazaar has served over 10,000 retailers in Karachi and has a catalogue of over 500 SKUs on its platform.

As their first product, Bazaar created a mobile-based B2B e-commerce marketplace that enables kiryana stores to purchase directly from manufacturers, wholesalers, and suppliers. The Bazaar App provides kiryana owners with a large assortment of branded and unbranded products, which can be ordered at any time, any day with free next-day delivery. On one end of the marketplace, kiryana owners benefit from Bazaar App’s convenient ordering, reliable delivery, and competitive prices. Suppliers, on the other end, get a direct-to-retail channel and are provided with actionable insights on purchase patterns and trends.

Sokowatch (East Africa)

A last-mile distribution platform, Sokowatch enables small shop owners to restock essential goods at the tap of a button. Using a basic mobile phone, shop owners send Sokowatch their orders and location, and salaried Sokowatch agents fulfil the orders from central distribution hubs, delivering them in two hours or less. Using its history of purchasing data, Sokowatch can predict incoming orders from shop owners and pre-stock tuk-tuks (a three-wheeled motorized vehicle) to ensure quick delivery. As shop owners place more orders, Sokowatch collects more data to plan its inventory and optimize its operation. Sokowatch also offers financing to these microentrepreneurs, and its use of predictive data helps it anticipate and plan for those needs as well.

MaxAB (Egypt)

Founded in 2018, MaxAB has built a digital platform to manage procurement and delivery of grocery products to shops in Egypt. The startup’s developer team created an app for store owners to purchase goods, another logistics app for its delivery fleet, and one for its customer support team. MaxAB’s target market is small-scale retailers in Egypt who sell to the country’s 100 million population; 90% of this $50 billion market gets transacted through small mom-and-pop shops. MaxAB has a fleet of 60 trucks and a large warehouse that serves Cairo. MaxAB has a staff of 270 and 9,000 retailers on its app, according to a company release. The venture generates revenue on margins it earns from the buy to sell price of the products it offers.

Merritt Hummer, TechCrunch – B2B marketplaces will be the next billion-dollar e-commerce start-ups (https://techcrunch.com/2020/11/04/b2b-marketplaces-will-be-the-next-billion-dollar-e-commerce-startups/)

Julia Morrongiello, Point9 – A Primer on B2B Marketplaces: Challenges and Opportunities (https://medium.com/point-nine-news/a-primer-on-b2b-marketplaces-challenges-and-opportunities-694a067cec91)

Julia Morrongiello, Point9 – The B2B Marketplace Stack (https://medium.com/point-nine-news/the-b2b-marketplace-stack-fa5b650f09b0)

Anu Hariharan and Nic Dardenne, Y Combinator – Reimagining B2B Commerce with Faire (https://blog.ycombinator.com/reimagining-b2b-commerce-with-faire/)

McKinsey & Co – How B2B online marketplaces could transform indirect procurement (https://www.mckinsey.com/business-functions/operations/our-insights/how-b2b-online-marketplaces-could-transform-indirect-procurement#)

Creandum – The decade of B2B marketplaces – and what we are looking for (https://blog.creandum.com/the-decade-of-b2b-marketplaces-and-what-we-are-looking-for-fdd116e67138)

Harvard Business Review – E-Hubs: The New B2B Marketplaces (https://hbr.org/2000/05/e-hubs-the-new-b2b-marketplaces)

Magento – The Rise of B2B Marketplaces (https://magento.com/blog/best-practices/rise-b2b-marketplaces)

Alibaba.com – What is a B2B marketplace? And the best way to utilise it (https://seller.alibaba.com/businessblogs/px601plc-what-is-a-b2b-marketplace-and-the-best-way-to-utilize-it)

Hokodo – Mum, why the f*** did I launch a B2B marketplace? (https://www.hokodo.co/blog/mum-why-the-f-did-i-launch-a-b2b-marketplace)

Disclaimer

This presentation is not an advertisement or a prospectus and is not intended for public use or distribution. It has been prepared by Sturgeon Capital Limited (“Sturgeon Capital”) for information and discussion purposes only with prospective eligible investors and should not be considered to be an offer or solicitation of an offer to buy or sell shares in the capital of the Fund. In particular, this document does not constitute an offer to sell, or the solicitation of an offer to acquire or subscribe for shares in the capital of the Company in any jurisdiction where to do so would be unlawful. This document, any presentation made in connection herewith and any accompanying materials do not purport to contain all information that may be required to evaluate the Company and/or its financial position and do not, and are not intended to, constitute either advice or a recommendation regarding shares of the Company. This document is not intended to provide, and should not be relied upon for, accounting, legal or tax advice and each prospective investor should consult its own legal, business, tax and other advisers in evaluating any potential investment opportunity.

The information in this presentation has not been fully verified and is subject to material revision and further amendment without notice. This presentation has not been approved by an authorised person in accordance with section 21 of the Financial Services and Markets Act 2000. As such this document is being made available only to and is directed only at: (a) persons outside the United Kingdom; (b) persons having professional experience in matters relating to investments falling within Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (the “Order”); or (c) high net worth bodies corporate, unincorporated associations and partnerships and trustees of high value trusts as described in Article 49(2) (A) to (C) of the Order, and other persons to whom it may otherwise lawfully be communicated (all such persons together being referred to as “relevant persons”). Any failure to comply with these restrictions constitutes a violation of the laws of the United Kingdom.

The distribution of this presentation in, or to persons subject to the laws of, other jurisdictions may be restricted by law and persons into whose possession this document comes should inform themselves about, and observe, any such restrictions. Any failure to comply with these restrictions may constitute a violation of the laws of the relevant jurisdiction. This presentation may not be copied, circulated or published, in whole or in part, without the prior written consent of Sturgeon Capital.

None of the Company or Sturgeon Capital or any other person makes any guarantee, representation or warranty, express or implied, as to the accuracy, completeness or fairness of the information and opinions contained in this document, and none of the Company or Sturgeon Capital or any other person accepts any responsibility or liability whatsoever for any loss howsoever arising from any use of this document or its contents or otherwise arising in connection therewith.

In preparing this presentation, Sturgeon Capital has relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources or which Sturgeon Capital otherwise reviewed. The information presented in this document may be based upon the subjective views of Sturgeon Capital or upon third party sources subjectively selected by Sturgeon Capital. Sturgeon Capital believes that such third party sources are reliable, however no assurances can be made in this regard.

Neither this presentation nor its contents may be distributed, published or reproduced, in whole or in part, by you or any other person for any purpose. In particular, neither this presentation nor any copy of it may be: (i) taken or transmitted into the United States of America; (ii) distributed, directly or indirectly, in the United States of America or to any US person (within the meaning of regulations made under the US Securities Act 1933, as amended); (iii) subject to certain exceptions, taken or transmitted into Canada, Australia, New Zealand or the Republic of South Africa or to any resident thereof; or (iv) taken or transmitted into or distributed in Japan or to any resident thereof. Any failure to comply with these restrictions may constitute a violation of the securities laws or the laws of any such jurisdiction. The distribution of this document in other jurisdictions may be restricted by law and the persons into whose possession this document comes should inform themselves about, and observe, any such restrictions.

The value of investments and the income from them can fall as well as rise. An investor may not get the amount of money he/she invests.

This document may include statements that are, or may be deemed to be, forward-looking statements. The words “target”, “expect”, “anticipate”, “believe”, “intend”, “plan”, “estimate”, “aim”, “forecast”, “project”, “indicate”, “should”, “may”, “will” and similar expressions may identify forward-looking statements. Any statements in this document regarding the Company’s current intentions, beliefs or expectations concerning, among other things, the Company’s operating performance, financial condition, prospects, growth, strategies, general economic conditions and the industry in which the Company operates, are forward-looking statements and are based on numerous assumptions regarding the Company’s present and future business strategies and the environment in which the Company will operate in the future. Forward-looking statements involve inherent known and unknown risks, uncertainties and contingencies because they relate to events and depend on circumstances that may or may not occur in the future and that may cause the actual results, performance or achievements of the Company to differ significantly, positively or negatively, from those expressed or implied by such forward-looking statements. No representation or warranty, express or implied, is made regarding future performance or the achievement or reasonableness of any forward-looking statements. As a result, recipients of this document should not rely on forward-looking statements due to the inherent uncertainty. Save as required by applicable law or regulation, the Company undertakes no obligation to publicly release the results of any revisions to any forward-looking statements in this document that may occur due to any change in its expectations or to reflect events or circumstances after the date of this document. No statement in this document is intended to be, nor should be construed as, a profit forecast.

This document includes certain track record information regarding Sturgeon Capital. Such information is not necessarily comprehensive and potential investors should not consider such information to be indicative of the possible future performance of the Company or any investment opportunity to which this document relates. The past performance of Sturgeon Capital is not a reliable indicator of, and cannot be relied upon as a guide to, the future performance of Sturgeon Capital or the Company.

By accepting this document or by attending any presentation to which this document relates you will be taken to have represented, warranted and undertaken that: (i) you are a relevant person; (ii) you have read and agree to comply with the contents of this disclaimer; and (iii) you will treat and safeguard as strictly private and confidential all the information contained herein and take all reasonable steps to preserve such confidentiality.